Visibility and the Formation of Exposure

Project controls present a coherent view of position - tracking cost, schedule and progress within structured reporting frameworks.

However, visibility within a system should not be confused with visibility of reality.

As projects progress, decisions are made under increasing pressure. Timelines compress, options narrow and assumptions begin to harden. These assumptions are carried forward as commitments form, often becoming embedded before they are fully tested.

The reported position may remain internally consistent, while gradually diverging from the underlying exposure.

As a result, exposure accumulates before it is formally recognised - forming at the point of decision, not reporting.

The Structural Limitation of Project Controls

Project controls operate within delivery. Their role is to provide structure and visibility across cost, schedule and performance.

They are not designed to report exposure as decisions are made. They provide visibility of position once commitments have already been taken.

By that stage, exposure may already be embedded, while controls continue to reflect a position that appears stable.

This is not a failure of project controls. It is a function of their design.

The Gap Between Control and Accountability

Accountability for capital outcomes remains with ownership. Boards, executives and asset owners carry responsibility for decisions, even where delivery is delegated and control systems are in place.

This creates a gap.

Controls provide visibility within delivery. Audit provides retrospective assurance. Advisory functions support specific interventions. Yet none of these operate consistently at the point where capital decisions are made and commitments become difficult to reverse.

The gap sits between these functions - at the point where exposure is created.

This is not a replacement for audit or project controls. It addresses a structural gap between them - at the point where capital decisions are made and exposure forms before it is visible in reporting.

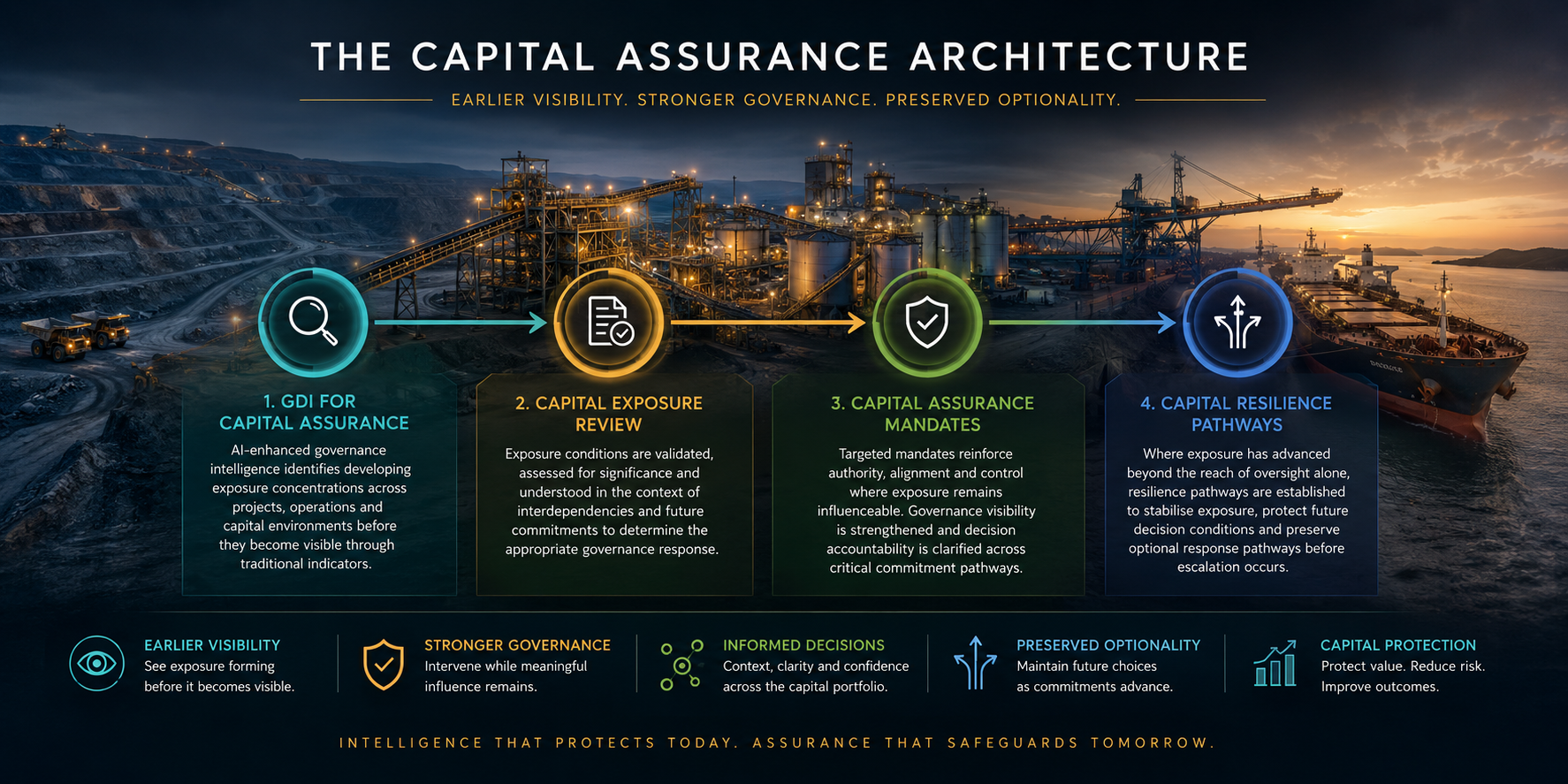

A Different Application of Governance

Addressing this gap does not require more reporting, additional controls, or further process overlay. It requires a different application of governance - one that operates where capital outcomes are determined.

Such an approach is applied at the point of decision, not after the fact. It focuses on whether exposure is forming as commitments are made, whether assumptions remain valid under pressure, and whether the position being relied upon continues to hold as conditions evolve.

In this context, governance operates above delivery systems - ensuring that the information and controls supporting decision-making remain reliable at the point where capital is committed. This aligns with principles established in ISO 37000, which place governance above management - focusing on direction, oversight and accountability rather than execution.

Why This Matters

Most capital loss does not occur because systems fail. It occurs because exposure forms before it is visible, while decisions are still being made under pressure and before positions become constrained.

Once embedded, that exposure becomes difficult to unwind. Reporting and audit may eventually reflect the outcome, but by that point the trajectory is largely set.

Effective governance therefore depends not only on structured information, but on whether that information remains reliable at the point where decisions are made.

Governance does not replace project controls or remove uncertainty. It ensures that the decisions driving outcomes are made with full visibility of exposure before they become irreversible - when they can still be challenged.

The Question That Remains

The question is not whether structured project controls are in place.

It is whether the position they present remains true at the point where capital is being committed - and whether exposure is being understood before it becomes irreversible.

What Sits Between the System and the Outcome

This gap is rarely addressed directly. It sits between established functions and is often recognised only once outcomes begin to drift.

It is not resolved through additional controls, expanded reporting, or traditional retrospective assurance. These remain within existing structures and rely on the same underlying assumptions.

Addressing this gap requires assurance applied at the point where capital decisions are made - while exposure is still forming and before positions become constrained.

This shifts assurance from retrospective review to application at the point of commitment, ensuring that the position being relied upon remains sound as decisions are taken.

In practice, this delivers confidence that the decisions committing capital are based on reality - not assumptions that only become visible later.